Contents

What are real estate notes?

In the United States, a mortgage note (also called a real estate lien note, lender’s note) is a promissory note secured by a specified mortgage loan. Mortgage notes are a written promise to repay a specified amount of money together with interest at a specified rate and length of time to fulfill the promise.

How do real estate papers make money?

What is the difference between a note and a mortgage?

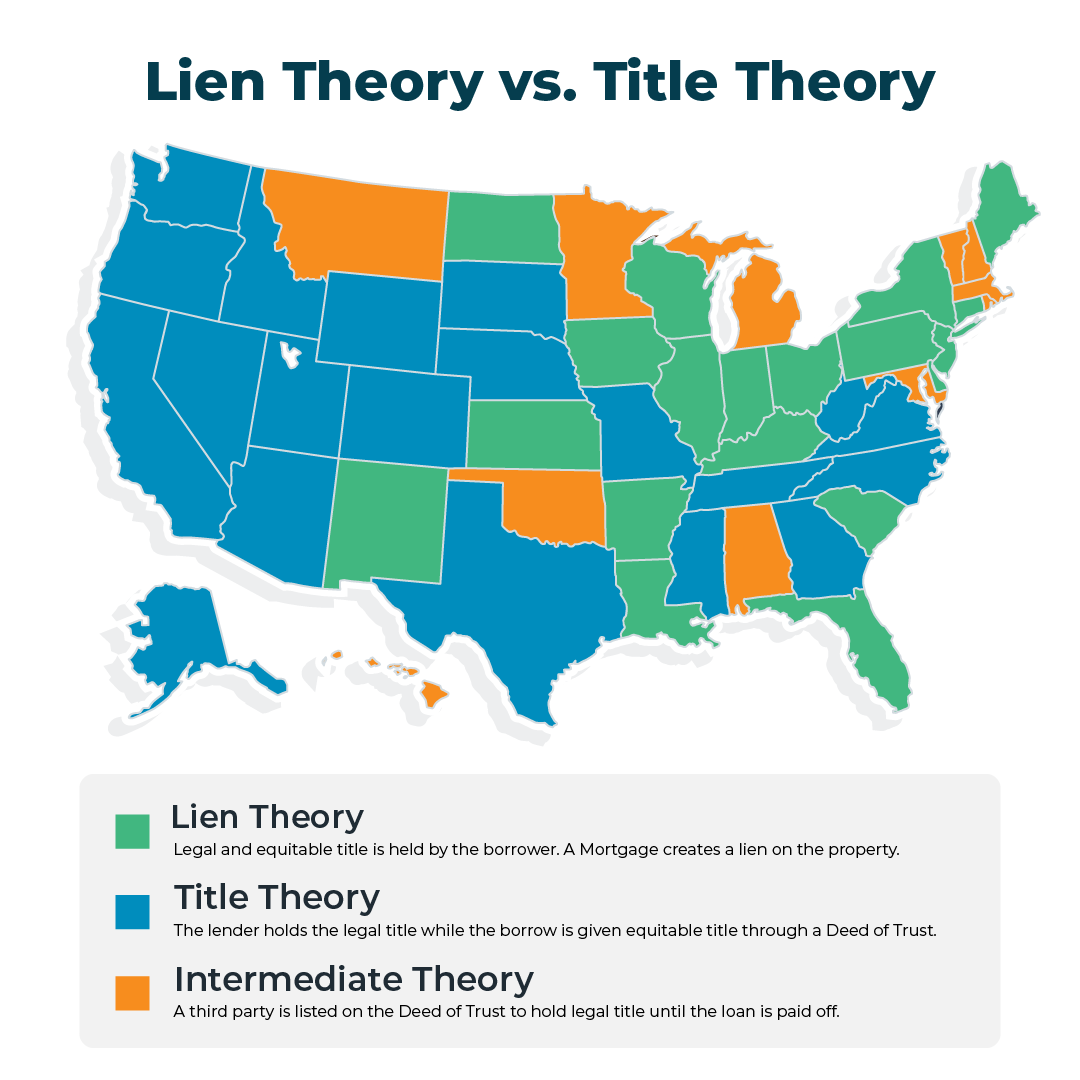

Promissory Note Vs. A mortgage. A promissory note is a document between the lender and the borrower where the borrower promises to pay the borrower back, it is a separate contract from the mortgage. The mortgage is a legal document that binds or “secures” a piece of real estate to an obligation to repay money.

Can you be on the note but not the mortgage?

But just because they’re on the Mortgage, doesn’t mean they’re on the Note. For example, one spouse will often have bad credit so they are not on the Note (lenders sometimes say ‘they are not on the loan’), but both spouses are on the Deed, so they have to both spouses being on the Mortgage.

Is a mortgage called a note?

A mortgage note is a legal document that sets out all the terms of the mortgage between a borrower and their lending institution. It includes terms such as: Total home loan. Down payment amount.

What is a mortgage loan officer?

A loan officer works for a bank or independent lender to assist borrowers in applying for a loan. Since many consumers work with loan officers for mortgages, they are often referred to as mortgage loan officers, although many loan officers help borrowers with other loans as well.

What is the difference between a mortgage broker and a loan officer? A loan officer works for a bank, credit union, or other mortgage lender, and will only offer the programs and mortgage rates available from that organization. A mortgage broker works on behalf of a borrower to find the best rate and loan from a number of institutions.

What skills does a mortgage loan officer need?

Key skills that contribute to the success of a mortgage loan officer:

- Love of working with people.

- Excellent communication skills.

- Strong analytical skills.

- Ability to sell.

- The ability to solve problems.

- Excellent attention to detail.

- Industry knowledge through annual continuing education.

What kind of math do loan officers use?

1. mathematics of money. 2. Scheduling or budgeting and mathematics accounting.

What makes a good MLO?

Ultimately, as a lender you will want words like ‘reliable,’ responsive, knowledgeable, helpful to be words that describe your services to future clients and professional relationships. Invest in your relationships so people see you this way.

What is the difference between a loan officer and an underwriter?

Your loan officer will then pass the application on to the underwriter, who will assess your creditworthiness. If the guarantor approves your loan, your loan officer will then collect and prepare the appropriate loan closing documents.

Is a loan officer the same as underwriter?

The guarantor works with a loan processor to gather the necessary documents and may request updated documents if necessary. This application is usually made through the loan officer, who works with the applicant-borrower. It is unlikely that the applicant-borrower will ever come into contact with the guarantor.

What is the difference between underwriter and lender?

The key difference between a lender and an underwriter is that a lender takes financial risk by providing a loan (or other guarantee), while an underwriter determines the value of the risk, which is the core criteria for approving the loan and setting an interest rate.

Is being a mortgage loan officer stressful?

Like any job working with the public, being a loan officer can be stressful at times. If you can deal with that stress in a calm manner, your career as a loan officer is likely to be lucrative.

Is a loan officer a high stress job?

57: loan officer. With a median salary of $63,650, loan officers report an average level of job stress and upward mobility, according to the report, but also have an above-average level of flexibility and life balance and work.

Is it hard being a mortgage loan officer?

Being a Loan Officer Can Be Very Experienced First of all, it is not an easy job. Sure, a mortgage broker or bank might tell you it’s simple. And yes, you may not have to work very hard in the traditional sense, or engage in any back-breaking work.

Can I sell my mortgage to someone?

In most circumstances, a mortgage cannot be transferred from one lender to another. That’s because most lenders and loan types don’t allow another borrower to take over an existing mortgage payment.

How does taking over someone’s mortgage work? An assumed mortgage allows a buyer to take over the seller’s mortgage. Once the assumption is complete, you take over the payments on a monthly basis, and the person you are taking the loan from is released from further obligation.

Can I sell my mortgage?

The short answer is yes. You can sell your home even if it has a balance on the existing mortgage. In fact, this is common. Outside of refinancing, this is probably the second most common way to pay off a mortgage because more people have a mortgage than own their property free and clear.

Can you sell house without paying off mortgage?

Yes, you can sell your house before paying off your mortgage. Mortgages range from 10 to 30 years so most homes sold in the US are not paid off in full. “Most of my sellers have a mortgage,” says Knoxville, TN agent Rebecca Carter.

What happens if you want to sell your house with a mortgage?

When you sell your home, the buyer’s funds pay your mortgage lender and cover transaction costs. The remaining amount becomes your profit. That money can be used for anything, but many buyers use it as a down payment for their new home.

Can someone buy you out of your mortgage?

A mortgage purchase is when one property owner pays the other owner’s share of the property’s equity, so that the co-owner can be released from the mortgage and removed from the deed as owner.

How is mortgage buyout calculated?

To determine how much you have to pay to buy out the house, add your ex’s equity to the amount you still owe on your mortgage. Using the same example, you would need to pay $300,000 ($200,000 remaining mortgage balance $100,000 ex-spousal equity) to buy out your ex-spouse’s equity and take ownership of the house.

How does someone buy you out of a house?

In most cases, a purchase goes hand in hand with refinancing the home mortgage loan. Usually, the buying spouse applies for a new mortgage loan in that spouse’s name only. The buying spouse takes out a loan large enough to pay off the previous loan and pay what the selling spouse owes on the purchase.

Can a loan be transferred to another person?

Key Takeaway. In most cases you cannot transfer a personal loan to another person. If your loan has a cosigner or guarantor, that person will be responsible for the debt if you default on the loan. Defaulting on a personal loan is very damaging to your credit score.

Can you transfer car loan to another person?

You cannot “transfer” a car loan to someone else without also transferring ownership of the vehicle to them. In most cases, a transfer of ownership is considered a sale.

Can home loan be transferred to another person?

Yes, a home loan can only be transferred from one person to another if the property owner decides to sell the property to a new buyer.

Why do banks sell mortgages?

The answer is fairly simple. Lenders usually sell loans for two reasons. The first is to free up capital that can be used to make loans to other lenders. The other is to generate cash by selling the loan to another bank while retaining the right to service the loan.

Why are banks allowed to sell mortgages? Your lender may also sell your loan as a way to free up capital. When banks sell loans, they are actually selling the servicing rights to them. This frees up lines of credit and allows borrowers to transfer money to other lenders (and make money on the mortgage origination fees).

What does it mean when a bank sells your mortgage?

Having a loan sold means that the borrower has sold the rights to service the loan (ie collect the monthly principal and interest payments.) Everything about the loan remains the same except the address the mortgage payments are sent to him. There are several reasons why mortgage lenders sell loans.

Is it common for banks to sell mortgages?

It is very common for mortgage loans to be sold, and it is not alarming. You should receive a notice in the mail before and after the sale.

Can you stop a bank from selling your mortgage?

Can you prevent your mortgage from being sold? No, you do not have the ability to prevent your mortgage from being sold.

How do banks make money by selling mortgages?

Mortgage lenders can make money in a variety of ways, including origination fees, product spread premiums, discount points, closing costs, mortgage-backed securities (MBS), and loan servicing. Closing cost fees that lenders can make money from include application, processing, underwriting, loan lock, and other fees.

How much do banks make when they sell a mortgage?

Origination fees are usually charged at a rate of between 0.5 and 1% of the mortgage value. So, on a house worth $380,000 you would pay $1900 if the origination fee is calculated at 0.5% and $3,800 at a rate of 1%. The average interest rate on a mortgage in the USA is 3.99% on a 30 year fixed rate mortgage.

Is it common for banks to sell mortgages?

It is very common for mortgage loans to be sold, and it is not alarming. You should receive a notice in the mail before and after the sale.

Why do mortgages get sold so often?

In the hope of making a quicker profit, lenders will often sell the loan. If servicing a loan costs more than the money it brings in, lenders can try to sell the servicing to reduce their costs. The borrower can also sell the loan itself to free up money to make more loans.

Is it common for mortgages to be sold?

It is very common for mortgage loans to be sold, and it is not alarming. You should receive a notice in the mail before and after the sale.

How many times do mortgages get sold?

“Sometimes, a mortgage loan can be sold multiple times without the borrower’s knowledge if the servicer does not change with the sale,” Whitman said. If your loan is sold or transferred and the servicer changes, here’s what to expect and do: Expect to receive two notices. One will come from your current service provider.

Sources :

Comments are closed.